It is an information affidavit established in subclause 15.3 of Section 87 of the Single Revised Text (TUO, for its Spanish acronym) of the Tax Code, containing the information of the beneficial owner.

Legal Basis: Subparagraph b) of paragraph 3.1 of Section 3 of Legislative Decree 1372.

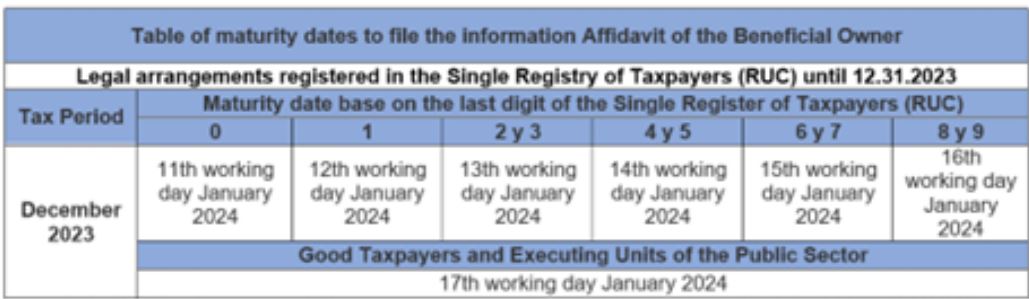

Term for filing the affidavit

The filing of the affidavit by liable taxpayers will be gradually made.

In years 2022 to 2024, as set forth in subparagraphs a) (legal persons) and b) (legal arrangements) of Section 2 of 000041-2022/SUNAT

, liable taxpayers shall file the beneficial owner’s information to SUNAT, as detailed below:

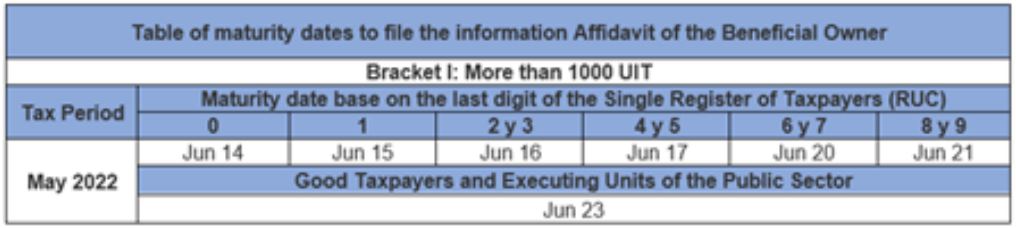

- The informative affidavit of the Beneficial Owner corresponding to Bracket I (legal persons declaring net income exceeding 1000 tax units (UIT) with regard to period 2021), in the month of June and taking into consideration tax period May 2022 (*) as the deadline.

(*) Established in Appendix I of Superintendence Resolution N. º 000201-2021/SUNAT

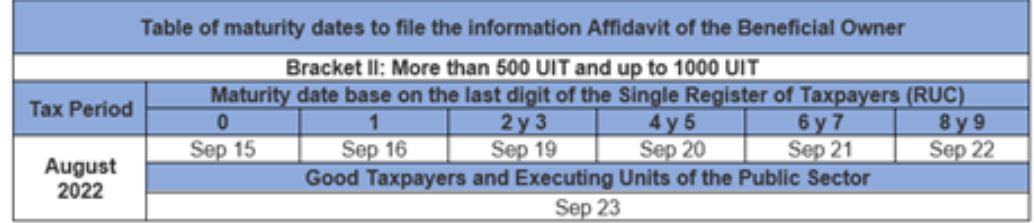

The informative affidavit of the Beneficial Owner corresponding to Bracket II (legal persons declaring net income exceeding 500 tax units (UIT) to 1000 tax units (UIT) with regard to period 2021), in the month of September, and taking into consideration tax period August 2022 (*) as the deadline.

(*) Established in Appendix I of Superintendence Resolution N. º 000117-2022/SUNAT

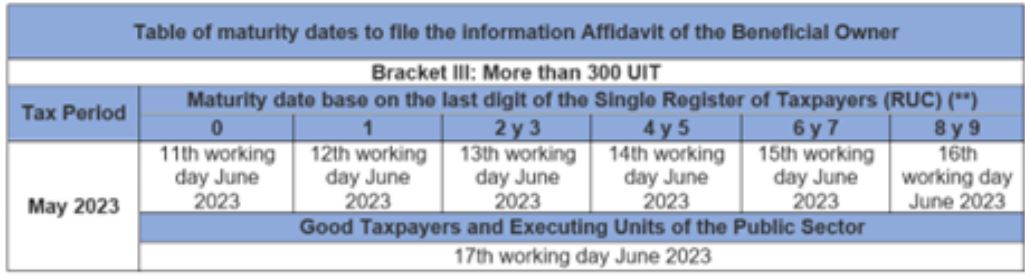

- The informative affidavit of the Beneficial Owner corresponding to Bracket III (legal persons declaring net income exceeding 300 tax units (UIT) with regard to period 2022), in the month of June, and taking into consideration tax period May 2023 (*) as the deadline.

(*) Established in Appendix I of Superintendence Resolution N. º 000117-2022/SUNAT

- The informative affidavit of the Beneficial Owner corresponding to Bracket III (legal persons declaring net income exceeding 300 tax units (UIT) with regard to period 2022), in the month of June, and taking into consideration tax period May 2023 (*) as the deadline.

(*) Established in Appendix I of Superintendence Resolution N. º 000281-2022/SUNAT

Liable taxpayers that shall subsequently file the affidavit

- Liable taxpayers not addressed in Superintendence Resolutions 185-2019/SUNAT, 000041-2022/SUNAT and 000278-2022/SUNAT shall file the affidavit in the term established by SUNAT through Superintendence Resolution.

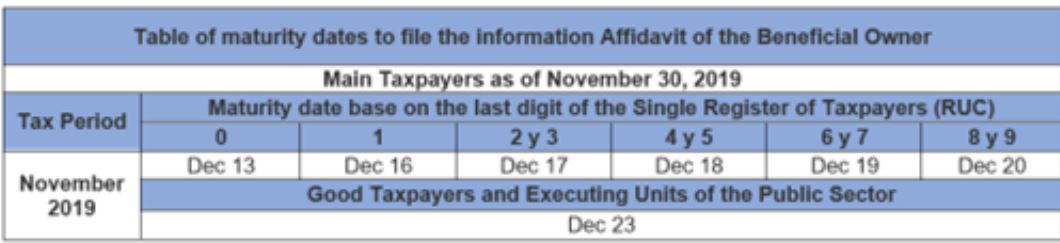

Background:

In 2019, as stated in paragraph 5.2, subparagraph 5 of Superintendence Resolution 185-2019/SUNAT, the first group of taxpayers liable to file the informative affidavit of Beneficial Owner were:

- Legal persons which have the status of main taxpayers as of November 30, 2019, shall file the affidavit containing beneficial owner information as of that date.

Also, it has been established that such affidavit shall be filed in December, and the deadline should be the date established in Appendix I of Superintendence Resolution 306-2018/SUNAT

for tax liabilities requiring monthly payments and corresponding to tax period November 2019. Therefore, the following deadline schedule was established:

1. UESP: Executing Units of the Public Sector.

Superintendency Resolution No. 168-2025/SUNAT established the deadline for certain obligated entities not included in the Superintendency Resolutions No. 185-2019/SUNAT and No. 41-2022/SUNAT to file the Ultimate Beneficial Ownership Declaration.

In the previously mentioned Superintendency resolutions, the filing of the Ultimate Beneficial Ownership Declaration based on the income earned by taxpayers was gradually implemented.

In order to continue gradually implementing the filing of the Ultimate Beneficial Ownership Declaration, the resolution published on May 28, 2025, establishes the deadline for certain obligated entities to file the informative declaration of their Ultimate Beneficial Owners.

Deadline to file the Ultimate Beneficial Ownership Declaration:

Legal entities domiciled in Peru, in accordance with the provisions of Article 7 of the Income Tax Law that are not considered in paragraph 5.2 of Article 5 of the Superintendency Resolution No. 185-2019/SUNAT or in subclause a) of Article 2 of Superintendency Resolution No. 000041-2022/SUNAT, file the Ultimate Beneficial Ownership Declaration:

Before the deadlines provided for in the schedule to meet the tax obligations for the tax period corresponding to their net income:

Bracket | Net Income | Deadline to file: Period |

1 | More than 100 Tax Units | October 2025 |

2 | More than 50 Tax Units up to 100 Tax Units | December 2025 |

3 | More than 25 Tax Units up to 50 Tax Units | July 2026 |

4 | More than 10 Tax Units up to 25 Tax Units | September 2026 |

5 | Up to 10 Tax Units | November 2026 |

Before the deadlines provided for in the schedule to meet tax obligations for the November 2026 tax period in the following cases:

- If legal entities are not required to submit all the determinative tax return referred to in subclause c) of Article 4.

- If legal entities are not included in any of the brackets referred to in section i).

- If entities have obtained their Tax ID (RUC) number before December 31, 2024, and have not activated it until that date.

- If entities are registeredin the Single Taxpayer Registry (RUC) or obtain the Tax ID number and activate it, if the activation is necessary, from January 1, 2025, until November 30, 2026.

Legal entities incorporated in Peru and registered in the Single Taxpayer Registry (RUC) from October 1, 2024 to November 30, 2026, whose Tax ID (RUC) number has not been deregistered as of the date when these are required to file the referred Declaration, must file the Declaration before the deadlines provided for in the schedule to meet monthly tax obligations for the November 2026 tax period.

Legal entities domiciled in Peru, in accordance with the provisions of article 7 of the Income Tax Law and legal entities incorporated in Peru that are registered in the Single Taxpayer Registry or obtain the Tax ID (RUC) number after November 30, 2026, must file the Declaration before the deadlines provided for in the schedule to meet tax obligations for the tax period in which they register in the Taxpayer's Registry or activate their Tax ID (RUC) number, if activation is necessary.

Calculation of net income:

For the calculation of the net income referred to in paragraph i) of subclause a) of article 3, the following must be considered:

If during the taxable year prior to the year on which the entity was required to file the Declaration, the legal entity was subject to the General Income Tax Regime or in the MSE (Micro and Small Enterprise) Tax Regime, then the net income shall be based on the highest amount resulting from the following operations:

The sum of the amounts entered in boxes 461 (net sales or revenue from services), 473 (taxed financial income), 475 (other taxed income), 476 (other non-taxed income) and 477 (disposal of securities or fixed assets) of the Virtual Form No. 710: Simplified Annual Income – Corporate Income or Virtual Form No. 710: Annual Income – Complete – Corporate Income and Tax on Financial Transactions (ITF).

The sum of the amounts entered in boxes 100 (taxed net sales), 105 (non-taxed sales), 112 (other sales), 127 (exports shipped during the period) and 160 (Sales, Law No. 27037) minus the amounts entered in boxes 102 (discounts granted and sales returns), 126 (discounts granted and/or sales returns – sales borne by the State and 162 (discounts and refunds, Law No. 27037) of the Form No. 621 VAT – Monthly income through Declara Fácil Platform (“Easy” Tax Filing Platform) or if applicable, of Online Tax File (PDT) N° 621 VAT - Monthly Income.

The sum of the amounts entered in box 301 (net income) of the Form No. 621 VAT – Monthly income through Declara Fácil Platform (“Easy” Tax Filing Platform) or, if applicable, those of the Online Tax File (PDT) N° 621 VAT - Monthly Income.

If in one or more periods of the taxable year prior to the year on which the entity was required to file the Declaration, the legal entity was subject to the Special Income Tax Regime, and subject to, among others, the General Income Tax Regime or the MSE (Micro and Small- sized companies) Tax Regime, the amount considered as net income will be the higher value resulting from the following operations:

The sum of the amounts entered in the boxes specified by the previously indicated subclause a) subsection i), plus the sum of the amounts included in box 301 (net income) of the Form No. 621 VAT – Monthly income through Declara Fácil Platform (“Easy” Tax Filing Platform) or of the Online Tax File (PDT) N° 621 VAT - Monthly Income of the monthly payments of the Special Income Tax Regime, corresponding to the period(s) in which the entity was subject to the Special Income Tax Regime.

The sum of the amounts entered in the boxes specified by the previously indicated subclause a) subsection ii).

The sum of the amounts entered in the boxes specified by the previously indicated subclause a) subsection iii) corresponding to the monthly instalments of the Special Income Tax Regime and income tax prepayments of the period(s) in which the entity was subject to the Special Income Tax Regime and the General Income Tax Regime or in the MSE (Micro and Small-sized companies) Tax Regime, where applicable.

For the purposes of the operations indicated in sections a) and b), in order to establish whether the legal entity is included in any of the Brackets to which the subclause a) of the article 3 refers to, the annual income tax return corresponding to the 2024 taxable year and the monthly returns for the periods January to December 2024, that are filed until October 31, 2025, including the rectifying returns that become effective up to that date, should be considered.

Non-domiciled legal entities and legal entities incorporated abroad must file the Ultimate Beneficial Ownership Declaration before the deadline established by SUNAT through a Superintendency Resolution.

Net Income estimation for determining the Brackets