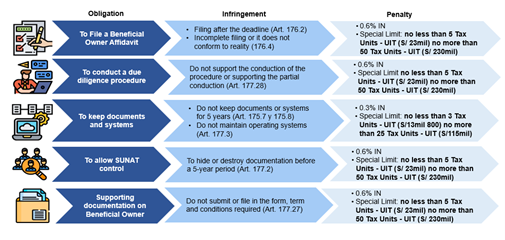

If the obligations related to the Beneficial Owner Affidavit, the due diligence procedure, safekeeping of supporting documentation and systems, and control from SUNAT are not met, the liable taxpayer will incur in penalties detailed as follows:

Note: The UIT used in the previous table corresponds to the year 2022 (S/ 4,600.00).

Amendment of Section 180 of the Consolidated Text of the Tax Code is considered which establishes special limits on sanctions related to the provision of Beneficial Owner information.

Please remember that the above-mentioned penalties are progressive if they are amended voluntarily as set forth in Superintendence Resolution 063-2007/SUNAT (except for those mentioned in paragraph 27 and 28 of article 177).